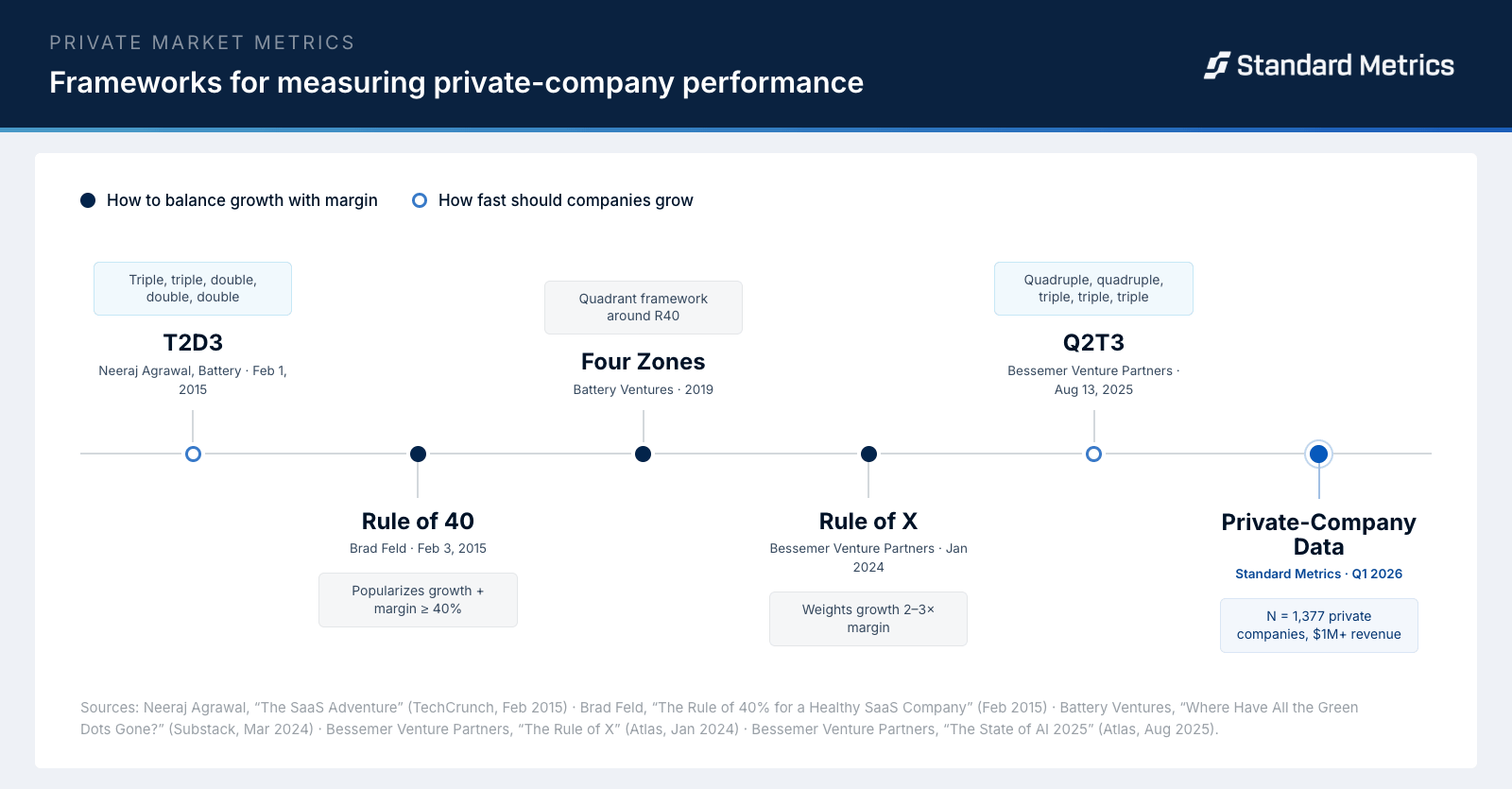

When private companies clear the Rule of 40, 89% of them do it through growth alone. Only 11% do it through balanced growth and margin — the profile the framework was originally designed to reward. That’s just one finding from our latest Private Market Report, focused on all things Rule of 40.

Every past analysis of the Rule of 40 was built on public data or small private portfolios. We ran it on 1,377 venture-backed private companies with $1M+ in annualized revenue. We examine where companies actually land across the four zones, how the distribution has shifted since 2021, what AI changes about the mechanics within each zone, and what the trajectory looks like as companies grow.